Now that we have examined a hypothetical 4 stock portfolio formed using quality as an assessment, we see that quality stocks can perform well even when handicapped (I picked 4 stocks in 1985 that were due to have one or more significant issues over the years between 1985 and 2023). This outperformance is despite the portfolio having a higher valuation than the S&P500 did in 1985 when the stocks or the index were bought. The S&P500 had a P/E of 11.0 and the 4 stock portfolio had an average P/E of 12.4. Now we are going to look at a major driver for the outperformance of quality stocks – their ability to earn above average returns on capital. The key to the 4 stock portfolio analyzed in the previous post was that these were all high long-term return on capital businesses at the outset. The 2 best performers were able to maintain high returns on capital over the 39 year investment period, despite running into trouble at times. The 2 bottom performing stocks perhaps maintained high returns on capital for a time, but suffered declines in return on capital. Durable and sustainable high returns on capital are a critical factor in what makes a stock high quality. Stocks that can maintain high returns on capital over time are highly likely to outperform regardless of starting valuation.

To understand this, I have put together 4 scenarios for very simple hypothetical businesses. These businesses only require capital and debt to purchase machines that make a product to sell. They don’t require pension plans or labor or other complicating factors. I have picked these hypothetical scenarios to illustrate the power of return on capital. Company A earns a high return on capital and is able to re-invest all returns and take out new debt in the amounts it desires to fuel its growth. This would be the case in an industry where the company has not yet saturated its market completely. It maintains its debt to equity ratio at 1. Company B earns the same a high return on capital, but is only able to reinvest the earnings it gets back into the business. It has no need to take out new debt to fuel its growth, so the debt level remains constant, while the equity capital grows (initial invested capital + retained earnings from each year it is in business). It’s debt to equity ratio starts out at 1 and approaches 0 over time as equity becomes much larger than the constant amount of debt. Company C earns a lower return on capital but is otherwise in the same situation as company A (it can grow as much as it feels comfortable taking on debt). Company D earns the same lower return on capital as company C and is in an industry that is slower growing, so, like company B it reinvests only its earnings into growth and does not take on additional debt. These situations are summarized in Table 1 below.

| High return on capital (15%) | Low return on capital (5%) | |

| Takes on new debt Debt/Equity =1 Leverage = 2X | Company A (Return on equity = 30%) | Company C (Return on equity = 10%) |

| Does not take on new debt Debt/Equity declines from 1->0 over time Leverage declines from 2->1 over time | Company B (Return on equity starts at 30%, declines to 15% over time) | Company D (Return on equity starts at 10%, declines to 5% over time) |

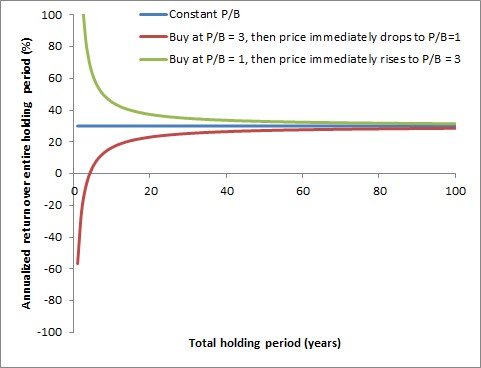

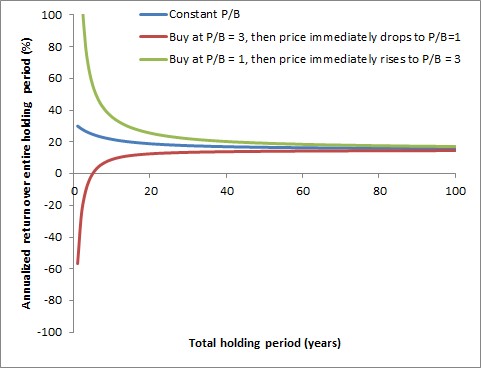

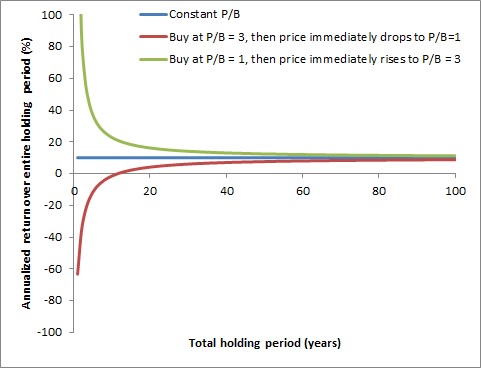

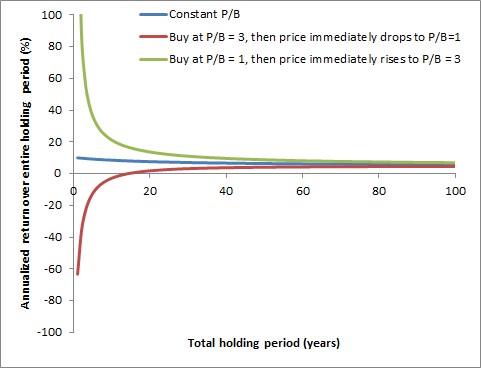

What do these 4 scenarios look like? Well, regardless of starting valuation, your return on these investments when you purchase the stock of company A, B, C, or D asymptotically converges to either the return on capital or the return on equity over time. Many people think that in order to make money in stocks you must buy an undervalued stock and then wait until it changes in valuation over time (to fully valued or overvalued). This is not true. The figures below show the average annualized return over time on your stock assuming different changes in valuation immediately after you buy the stock, either: 1) constant Price / Book (high or low doesn’t matter), 2) high price to book when you buy the stock and then the price / book ratio drops immediately after you buy the stock (you buy at a high valuation and then the valuation drops to a low valuation), or 3) low price to book when you buy and then the price to book ratio immediately rises to a higher value right after you buy (you buy at a low valuation and then the stock permanently remains at a higher valuation). As you can see from the graphs, it doesn’t really matter at what valuation you buy if you hold for long periods of time. Your average annualized return over the entire holding period converges to a single value the longer you hold.

That value your return converges on is the return on capital in the case where you do not take on new debt, and it is the return on equity if you do take on new debt (keeping the debt to equity ratio the same over the entire holding period for illustration purposes). The return on equity and return on capital are related by the following formula:

Return on Equity = (Return on Capital) X Leverage

So, if your return on capital is 10%, and your return on equity is 20%, your leverage must be 2X. That is, your (equity + debt) / equity = 2. In the examples above, all companies start out with a leverage of 2X. However, companies A and C continue to take new debt on to maintain leverage at 2X. Their capital structure remains constant. Companies B and D do not take on additional debt as the equity value grows with retained earnings, so the leverage starts out at 2X and declines over time to 1X as debt becomes negligible relative to equity.

Keep in mind, there are companies that can earn a high return on equity while having a low return on capital, but they must use excessive leverage to do so. Therefore, if 2 companies have the same return on equity, but one has a higher return on capital, it will always be preferable to the lower return on capital company, assuming all other factors are equal. This is why it is essential to pay attention to return on capital.

Further, you want to understand the return on capital of the underlying economic engine of the business, not the extraneous stuff, like whether the company sold off some real estate it wasn’t using. Companies that are selling off un-needed stuff can look like they have high returns on capital for a time, but this will fall back down when they finish the operation. You want to strip everything extraneous out of this calculation except for the stuff that matters – what the company’s core business or businessess are doing. If you can locate a business with durable and sustainable high returns on capital that aren’t eroded over time, your returns over longe enough periods of time will be excellent regardless of changes in valuation over time. Valuations in the real world have limits, and do not increase or decrease without bounds, so return on capital (or equity) will always dominate over time. This is precisely what Warren Buffet means when he says “It is better to own a great company at a good price than a good company at a great price.” It is also by the way, why Charlie Munger was able to convert him over almost exclusively to buying high quality businesses at good prices, when his old method consisted of a lot more of the classical Benjamin Graham style investing plays – buying “Cigar butts with one last puff”. That is, crappy businesses selling for less than the cash they have in the bank, where you could make money if they either righted the ship or closed up shop and distributed the cash.

That being said, you do of course want to buy businesses at reasonable valuations, because, as you can see from the charts above, it can take quite a long time to overcome an extremely high valuation at the time of purchase. My point is that you want the headwind of high return on capital to help you for the stocks that you purchase. We will cover valuation in the next post.

Finding high return on capital businesses with sustainable returns on capital that won’t erode over time is the trick. There aren’t many businesses out there that pass the test. There might be less than 5% of businesses that are truly like this. You want to look for the especially good companies (the top 0.1 – 1%). The average return on capital of the S&P500 has been about 7-8% over the last 20 years. I cannot find readily available data from earlier times, but it was likely a bit lower than this in previous years, due to smaller profit margins. Profit margins have been growing over the last few decades due to lower cost of debt, plus globalization and just in time supply chains creating more efficient businesses. The robustness of globalization and just in time supply chains has shown some problems in the post-Covid world, so re-shoring, and storing of more inventory seems to be ticking up. These may reverse the return on capital trend for a while, but overall, the trend is probably steady to slightly upward over long periods of time as we gain in efficiency and technology.

Given the return on capital of the S&P500 is 7-8%, you should be targeting businesses with a return on capital of bare minimum 10%, and 12% or higher would be best. A simple screener may be able to identify some of these for you, as well as looking through the list of dividend achievers, contenders and challengers. However, some of these gems will be hidden behind accounting quirks that only become apparent after you examine them deeper, so they will be missed by screens. These businesses tend to offer something that can be protected from competitors by high barriers to entry – brand names, patents, proprietary knowledge, outstanding management, high costs, regulatory capture, de-facto monopoly-like structure, etc. These are the businesses that you want to find for your Star List (your shopping list of high quality stocks).

Keep in mind that there are many businesses out there with a current high return on capital that is declining. This happens for a variety of reasons – poor decisions of management, changing markets, lack of new opportunities to invest capital in at similar high returns, and most importantly of all, the high returns are eroded by competition in the market. It cannot be emphasized enough that companies with sustainable high returns on capital have something special about them that allows them to keep those highly profitable businesses protected from forces acting to bring returns on capital down to earth. Some of these were mentioned above (brand names, patents, etc.). Keep in mind as you screen for businesses that there are many with a temporarily elevated return on capital, but you must weed these out in favor of businesses with a durable and sustainable high return on capital.

Now that we have discussed the idealized situation with 4 companies, let us bring it back to real world examples. Real companies can sometimes invest as much as they want into an area. That is, they haven’t yet saturated the market and/or the market is growing. Other times, they cannot really invest anything new into their high return on capital business. In-between situations can also occur. Similarly, early invested capital may have higher returns than later invested capital. So, real companies can have what is called an incremental return on capital. Further, the market structure, consumer tastes, government regulations, etc., can change over time, affecting returns on capital. Real companies can often have several businesses with different returns on capital, and so they have a blended return on capital. Real companies can seek out new opportunities that are either higher or lower in return on capital, depending on the ability and wisdom of management. If they seek out lower return businesses, then your returns will converge to the new lower average return on capital. If management foolishly and continuously repurchases its overvalued stock, long term returns can actually be lower than return on capital. Similarly, if management only repurchases stock when it is undervalued (think Berkshire Hathaway), your return can be higher than the return on capital. Your returns can be lower than the return on capital of the company if it issues dividends and you do not reinvest the dividends back into the company stock, instead spending them or reinvesting them into lower return businesses. Return on capital can be lower if management continuously and frivolously wastes valuable capital on vain or fruitless pursuits in an attempt to make it look like they are doing something to earn their pay.

While the situation for real world companies can be more difficult to disentangle, keep this in mind – over long periods of time, return on capital drives everything. Long-term returns are not driven by stock market sentiment. They are driven to diminishing extent over time by changes in valuation. Mathematically, returns must converge eventually to something driven by return on capital (note that return on equity is also driven by return on capital coupled with leverage).

Having the valuation change from undervalued to overvalued is not required for you to earn a fantastic return. In fact, you should hope and pray for a situation where you can invest in a high return on capital business that is perpetually undervalued for decades. With dividend reinvestment, share buybacks, and purchases of new stock, even if the true valuation was somehow never realized, you would have phenomenal returns and very soon become unbelievably wealthy. Permanent undervaluation would speed up this journey to fantastic wealth greatly – the valuation does not need to come back to average or become overvalued. Mathematically, it is unlikely for this situation to persist, however, or you would end up owning the entire company before long, so the valuation will almost always adjust back to normal eventually in order to prevent this situation. It can be very instructive to try running some simple scenarios of your own to see how this is the case.

Return on capital is an extremely important component of uncovering quality stocks that will have high future returns, and there are still several aspects of return on capital and related concepts that we have not yet discussed (for example, cost of capital which also figures into value creation). We will continue to explore these aspects in future posts.

Leave a Reply